In terms of biotechnological research, the United States are the world champion in inventions. But countries like Brazil and China are deploying them at a much faster pace, which should give them a considerable lead in the race for global food security. In 2026, the global hierarchy in agricultural biotechnology is marked by a consolidation of historical players (USA, Europe) and a meteoric rise of Asia‑Pacific. The global market, estimated at around 150 billion USD, is driven by climate urgency and food security.

The American lead is eroding in the implementation of new agricultural biotechnological inventions. The European Union, for its part, has succeeded in fast‑tracking regulations for genetically modified crops without foreign DNA, giving their biotech companies a decisive commercial advantage. Such is the alarm raised by American expert Ashal Shah. His thesis is summed up in the concise formula: America invents, Brazil and China deploy, and Europe sells.

China is fast. Chinese plantings of genetically modified corn and soybeans are said to reach three million hectares, four times the area of 2024. The Farmer and Rancher Freedom Framework, which defines the rights and freedoms of American farmers, attempts to remedy the legal and regulatory burdens in the United States. The use of Artificial Intelligence would be of great help.

Crops such as fruits and vegetables – which are not niche products – suffer dramatically from biotechnological underinvestment due to outdated American regulations.

A counter‑example, equivalent to China, is Brazil. Ashal Shah continues, in an article, that in the South American giant the market for biotechnological inputs jumped 15% during the 2023-2024 season and recorded an average annual growth of 21% over the last three years, four times the global average according to researchers from CEPEA in São Paulo.

The Brazilian 2024 law on biological inputs reduced approval times for biological products by 50% and its Plano ABC+ program reimburses up to half of farmers’ biological expenses. The result is that farmers deploy biological inputs in most of their crops, from soybeans and corn to sugarcane and coffee, still according to Ashal Shah.

If the United States were to remain a nation where only major traditional crops use biological inputs, half of the “healthy” part of the American plate would depend on imports, which would constitute a flaw in its food sovereignty, Ashal Shah fears. The 2026 U.S. farm bill, however, opens the door to measures that should improve “food sovereignty” in the United States.

Global Hierarchy

In 2026, the global hierarchy in agricultural biotechnology is marked by a consolidation of historical players (USA, Europe) and a meteoric rise of Asia‑Pacific. The global market, estimated at around 150 billion USD, is driven by climate urgency and food security.

Here is the current structure of this hierarchy, organized by geographic power and industrial dominance.

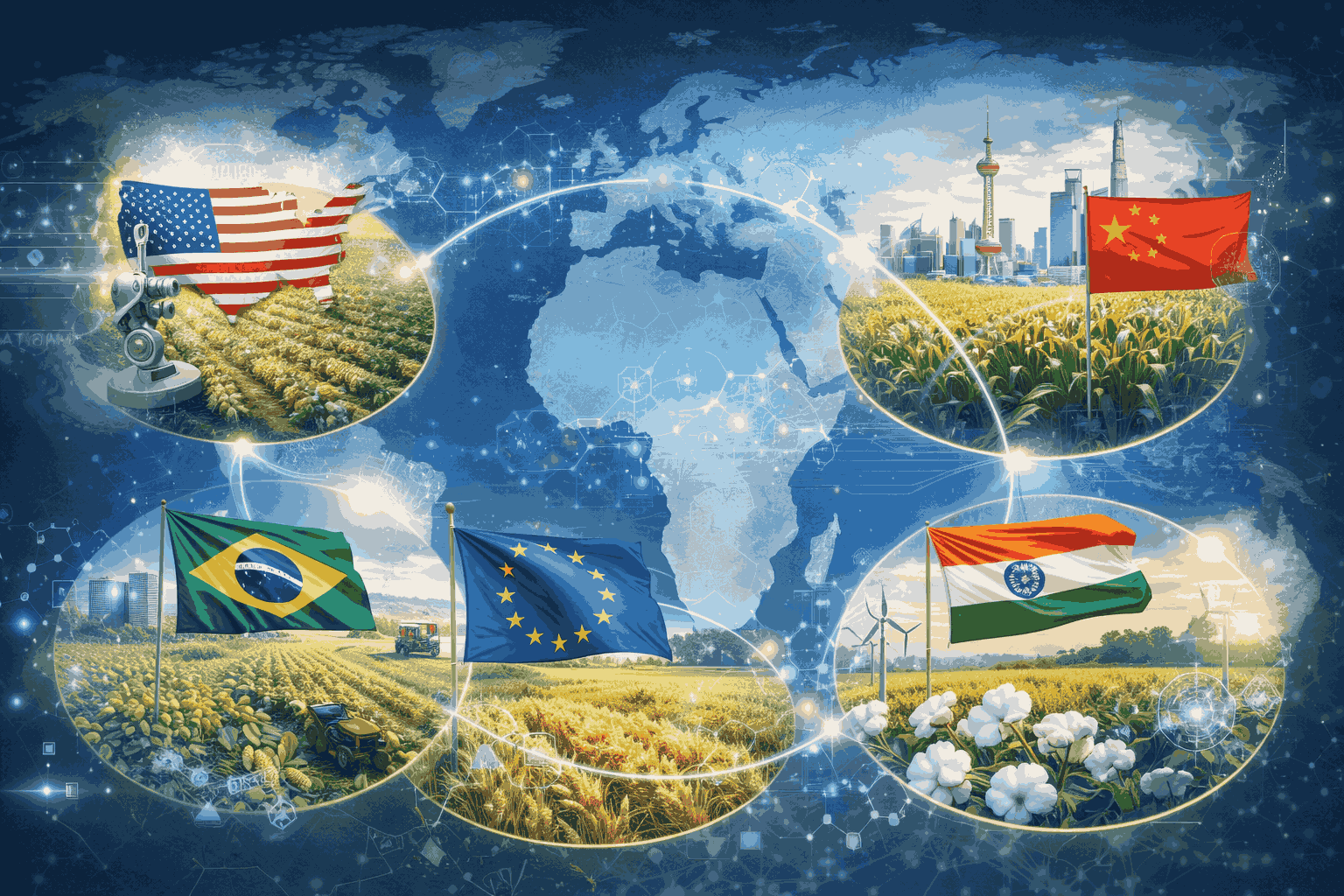

1. Geographic Powers: The Dominant Triad

The global hierarchy is divided into three major poles with distinct strategies:

| Region | Status | Key Assets |

|---|---|---|

| North America (USA/Canada) | Historical Leader | Holds the largest market share. Ultra‑performing R&D ecosystem and regulations favorable to CRISPR and genomic editing. |

| Asia‑Pacific (China/India) | Fastest Growth | Becomes the global engine in 2026. China invests massively in GM seeds for self‑sufficiency; India focuses on AI and biofertilizers. |

| Latin America (Brazil/Argentina) | Adoption Giant | Brazil is the 2nd largest producer of biotech crops (99% of its soybeans come from biotechnologies). |

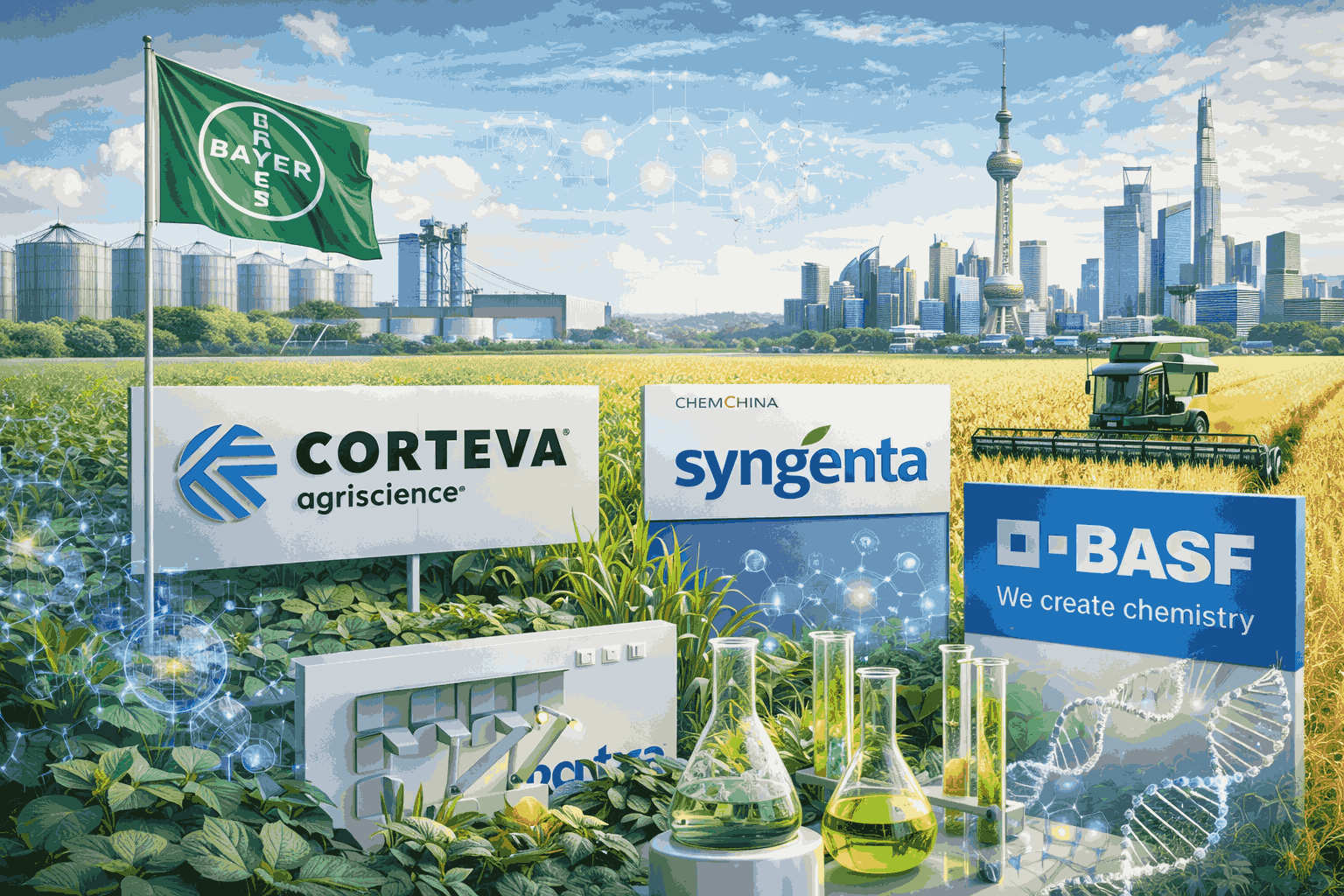

2. Industrial Leaders (The “Big Four”)

The sector is extremely concentrated. Four companies control the majority of patents and global distribution of seeds and biotech traits:

1. Bayer Crop Science (Germany/USA): Unchallenged leader since the acquisition of Monsanto. Dominates the market for GM seeds and herbicides.

2. Corteva Agriscience (USA): Resulting from the Dow‑DuPont merger, it is the global reference for drought resistance technologies (e.g., Acreon corn).

3. Syngenta (Switzerland/China): Owned by ChemChina, it bridges Western technologies and the booming Asian market.

4. BASF (Germany): Focused on chemical solutions combined with cutting‑edge biotechnological traits.

3. Disruptive Trends in 2026

The hierarchy is no longer just about “who sells the most GM soy.” It is being redefined by new segments:

• Genomic Editing (CRISPR‑Cas9): Unlike classical GMOs, these technologies (championed by companies like Calyxt or KWS) allow precise modifications without foreign DNA, facilitating their regulatory acceptance in Europe.

• “Biologicals”: The hierarchy shifts towards micro‑organisms. Leaders like Novonesis (merger of Novozymes and Chr. Hansen) dominate the biofertilizer and biopesticide sector, essential for reducing chemical use.

• Integration of AI: In 2026, a nation’s ability to couple biotech with AI (to predict yields or design plant proteins) becomes a marker of power, with a net advantage for the United States and India.

4. The Case of Europe: Influence through Standards

Although lagging in GMO cultivation, Europe (via France and Germany) remains at the top of the hierarchy thanks to its traditional seed giants (Vilmorin, KWS) and its ability to impose global standards in biosafety and “Green Tech.”

The agricultural biotechnology market is expected to double by 2035 to reach approximately 320 billion USD, with Asia‑Pacific as the main driver of this expansion.

Geographic Hierarchy

Here is a detailed hierarchy of power in agricultural biotechnology in 2026, classified by country and regional bloc, based on their innovation capacity, cultivated area, and regulatory weight.

1. The Undisputed Leader: United States

• R&D Capacity: Home to giants like Corteva and thousands of AgTech startups.

• Regulatory Advantage: A very liberal approach to genomic editing (CRISPR), considered non‑GMO if no foreign protein is introduced.

• Commercial Dominance: Leader in patents for corn, soybean, and cotton seeds.

2. The Systemic Challenger: China (and Asia‑Pacific)

• Sovereignty: Through the acquisition of Syngenta, China now has a global champion.

• Public Investments: The world’s largest public budget for plant biotechnology research.

• Expansion: In 2026, China massively accelerates the approval of GM corn and soybean varieties on its own soil.

3. The “Laboratories of the World”: The Mercosur Bloc (Brazil & Argentina)

• Brazil: Second largest producer of biotech crops in the world. It has become the leader in adopting new crop protection technologies.

• Argentina: Very advanced in developing drought‑resistant wheat (HB4), a world first exported to other countries in 2026.

4. The Normative Giant: The European Union

• Scientific Power: France (Vilmorin/Limagrain) and Germany (Bayer, KWS) remain world leaders in seed genetics.

• The “Brussels Effect”: Europe dictates global biosafety and traceability standards. In 2026, its decision to relax rules on NGTs (New Genomic Techniques) puts the European bloc back in the innovation race against the USA.

5. The Emerging Power: India

• Bioinformatics: Massive use of AI for plant genetic sequencing.

• Cotton and Mustard: After the success of Bt cotton, India has paved the way for other biotech food crops to feed its growing population.

BOX

State of Global Agricultural Biotechnology Research

In 2026, the state of global agricultural biotechnology research has entered an era of “extreme precision.” It is no longer just about modifying plants, but about designing cellular ecosystems capable of withstanding unpredictable climate shocks.

Here are the four pillars that define current research:

1. The Post‑CRISPR Era: NGTs (New Genomic Techniques)

Research has moved beyond simple genetic “copy‑paste.”

• Prime Editing: Researchers can now modify single nucleotides without breaking the DNA double helix, reducing unwanted mutations (off‑targets) to nearly zero.

• “Climate‑Native” Plants: The priority is no longer just yield, but multisensory resilience. Wheat and rice varieties are being developed to self‑adjust: they close their stomata faster during heat spikes or modify their root structure based on humidity detected by internal biological sensors.

• European Legalization: In early 2026, the EU’s adoption of a more flexible regulatory framework for category 1 NGTs (considered equivalent to conventional breeding) caused a massive influx of investments into French and German laboratories.

2. The Microbiome: The “Second Green Revolution”

Research has shifted from the plant to the soil.

• Living Fertilizers: Instead of modifying the plant to consume less nitrogen, synthetic micro‑organisms are created that fix nitrogen from the air ultra‑efficiently, directly on the roots of cereals (corn, wheat).

• Plant‑Microbe Communication: Recent studies in 2026 explore how to “reprogram” the chemical signals emitted by roots to attract specific bacteria capable of fighting pathogenic fungi without any chemical pesticides.

3. AI and Genomics Convergence (Deep Breeding)

Artificial intelligence is no longer just an analysis tool, but a design tool.

• Plant Digital Twins: Before planting a single seed, researchers simulate millions of genetic combinations in virtual environments reproducing the climatic conditions of 2040. This reduces the cycle of creating a new variety from 10 years to less than 3 years.

• Generative Protein AI: Models similar to those used for drugs are used to design plant proteins with a taste and texture identical to meat, directly integrated into the genetic code of legumes (peas, soy).

4. Research on Bio‑Safety and Ethics

Faced with the speed of advances, a growing part of research is dedicated to traceability.

• Molecular Markers: Development of invisible and harmless DNA “barcodes” to ensure that edited seeds do not spread uncontrollably in wild areas.

• IPES‑Food 2026 Report: A major global debate animates research on data concentration. Scientists are concerned about farmers’ dependence on the proprietary algorithms of biotech giants.

Summary of Priority Axes in 2026:

1. Tolerance to water and heat stress (World Priority #1).

2. Substitution of chemical inputs with biological solutions.

3. Biofortification (naturally increasing iron, zinc, or vitamins in staple crops).